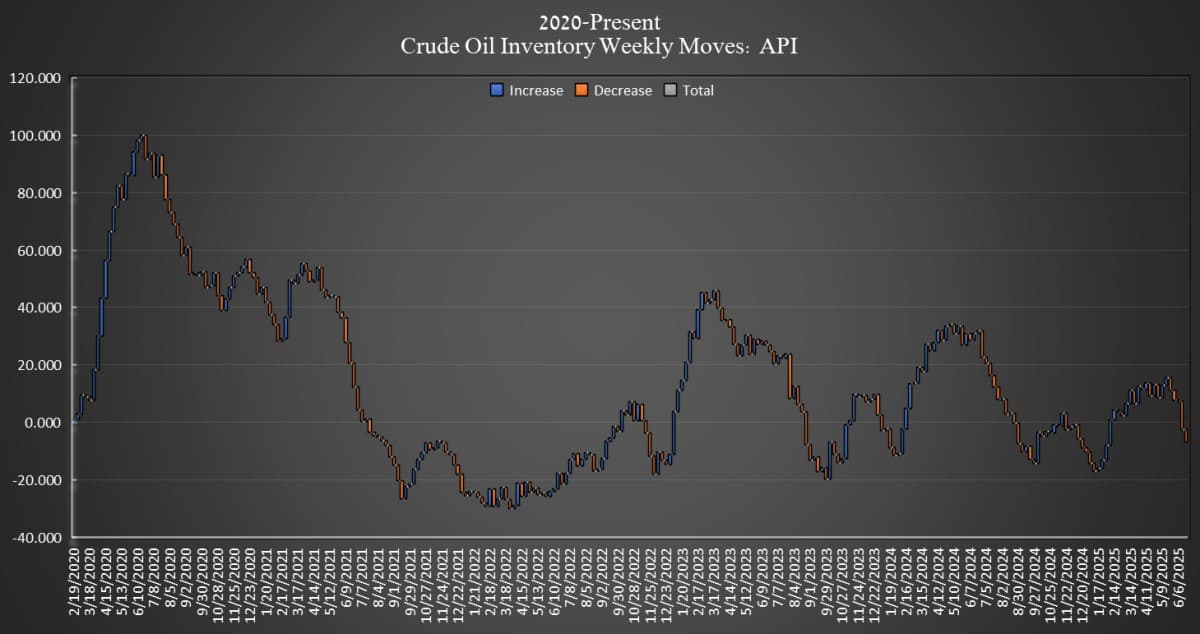

In a surprising turn of events, the landscape of the United States’ oil stockpiles has undergone notable fluctuations, underscoring the volatile nature of the energy sector. According to the American Petroleum Institute (API), a significant reduction was observed in the country’s crude oil reserves, which contracted by approximately 4.277 million barrels in the week that concluded on June 20. This development far exceeded the expectations set by analysts, who had anticipated a relatively modest decrease of 600,000 barrels. This recent contraction is in addition to the prior week’s extraordinary depletion of over 10.133 million barrels from the inventory, catching market observers and participants by surprise.

In the context of the broader timescale, the adjustments in inventory levels throughout the current year have been quite dynamic. According to calculations based on API data, despite these considerable weekly drawdowns, the cumulative inventory for the year has experienced a net increase of 3.3 million barrels. This attests to the complexity and unpredictable nature of global oil supply and demand dynamics, alongside the myriad factors—ranging from geopolitical tensions to global economic shifts—that influence them.

In parallel, a report emanating from the Department of Energy (DoE) earlier in the same week shed light on the state of the Strategic Petroleum Reserve (SPR). The SPR, a critical element in the U.S.’s energy security strategy, saw a slight uptick in its stock levels, with an increase of 200,000 barrels, bringing its total to 402.5 million barrels for the week ending June 13. This figure, while substantial, still falls significantly short of the inventory levels prior to the extensive withdrawals from the SPR under the administration of President Joe Biden, intended to stabilize market supplies and prices.

The repercussions of these inventory fluctuations were palpable in the trading markets as well. West Texas Intermediate (WTI), a crucial benchmark for U.S. crude, experienced a marked downturn in its trading price. Specifically, at 1:33 pm ET on the day in question, WTI’s value had descended by $3.99, a 5.82% decrease, settling at $64.52. This represented a sharp decline of approximately $8.50 from its price level the preceding week. Similarly, Brent crude, the global oil benchmark, was not immune to market pressures, witnessing a decrease of $4.15 (or 5.81%), which positioned its trading price at $67.33, more than $7 below its level the week before.

Turning attention to refined oil products, the fluctuations in inventories were equally noteworthy. Gasoline inventories, for example, saw an increment of 764,000 barrels in the week ending June 20, a reversal from the reduction of 20,000 barrels witnessed the week before. This adjustment brought gasoline stock levels to a point 2% below the five-year average for this time of year, as per the latest Energy Information Administration (EIA) data. Conversely, distillates, including heating oil and diesel, experienced a decrease in their inventories, with a draw of 1.026 million barrels, contrasting with a build of 318,000 barrels in the preceding week. This left distillate inventories 17% below the five-year average, which could have implications for market supply and pricing moving forward.

Of particular note is the situation at Cushing, Oklahoma, a pivotal hub for oil storage and the benchmark delivery point for U.S. futures contracts. Here, the inventory saw a reduction of 75,000 barrels in the week under review, following a more substantial decrease of 800,000 barrels the week before. These dynamics at Cushing are emblematic of the broader trends in U.S. crude oil stock levels, illustrating the continued volatility and unpredictability within domestic and global energy markets.

The nuanced shifts in oil inventory levels and their implications for trading prices are reflective of the broader economic and geopolitical landscapes that shape the global energy sector. Factors such as geopolitical tensions, changes in consumer demand, technological advancements, and regulatory changes play pivotal roles in influencing supply and demand dynamics. These recent developments in the United States’ oil inventory levels, set against the backdrop of broader market conditions, offer a compelling snapshot of the complex interplay between these factors and their collective impact on the energy sector at large. As market participants and observers look ahead, the ability to navigate and adapt to these fluctuations will be critical in shaping the future trajectories of oil markets, both domestically and globally.