The forthcoming period marks the onset of the second quarter of the fiscal year 2025 Earnings Season, positioning itself as a critical juncture for the global investment community. This phase sets in motion beginning next week, with a spotlight on the financial disclosures first made by major Wall Street banks. Such chronological unfolding of events paves the way for investors to recalibrate their expectations in the wake of financial performances unveiled by these corporate behemoths.

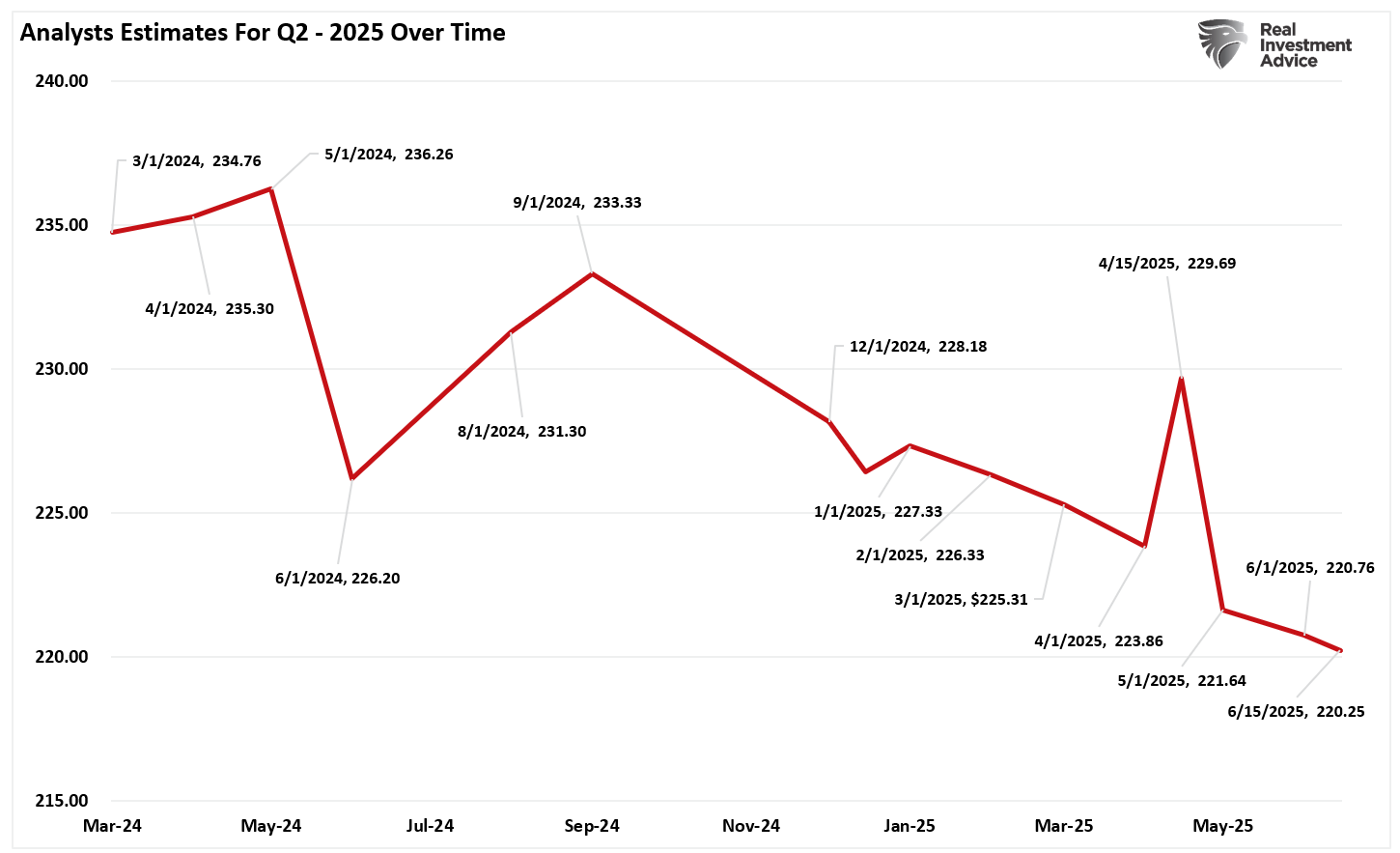

Delving into the heart of the matter, recent months have witnessed a palpable shift in Q2-2025 earnings forecasts. A projection made by S&P Global in March 2024, pegged the earnings at $234 per share, which later adjusted to $220 per share by 15th June 2025. This marked reduction is reflective of the caution among corporates, primarily stoked by tariff uncertainties that cloud their future economic assessments.

Adding a layer of complexity, FactSet insights revealed a trend where analysts have prudently scaled down their earnings projections for S&P 500 companies for the second quarter, more so than what’s historically averaged. Despite a lower frequency of companies providing negative earnings guidance, the anticipation for the quarter’s earnings remains subdued relative to the outset of the period, forecasting the lowest year-over-year earnings growth since the fourth quarter of 2023 at 4.0%.

The intensification of trade disputes, primarily during the tenure of President Trump, put pressure on market sentiments mid-year, with projections pointing towards a dip in EPS growth by approximately 1-2% per 5 percentage point increase in effective tariff rates. Although a respite from these tariffs is anticipated to extend into Q3, uncertainties persist, suggesting a strategic hedge against potential adversities.

A matter of significant concern trailing into Q2-2025 remains the slowing economic growth and its cascade effect on consumer spending. The Personal Consumption Expenditures (PCE) index serving as an economic indicator has shown a downtrend. Given PCE’s strong correlation with earnings, the downturn heralds possible repercussions on corporate earnings.

Moreover, the sectors of energy and materials have depicted a downturn in their earnings — about a 19% and 12% decline, respectively, year over year. This downturn is not an isolated phenomenon but rather signifies broader economic tepidness, concernedly watching these sectors as they are often mirrors of broader economic health.

Conversely, the technology and communication sectors, buoyed by considerable investments in artificial intelligence and capital expenditures, stand out as pillars of strength. These sectors, particularly giants renowned as the “Magnificent 7,” are anticipated to record robust earnings and revenue growth, potentially countering risks bleeding from trade ambiguities and dampened consumer dynamism.

As we edge closer to the earnings revelations, the approach of RIA Advisors delineates a strategy of prudence and recalibration. With markets swinging back to higher levels post the April downturn, sentiments are leaning towards ‘extreme greed,’ hinting at a heightened disposition for disappointments in the earnings announcements ahead. Thus, the strategy revolves around mitigating risks in the most vulnerable segments and enhancing cash reserves to capitalize on potential overreactions.

Our strategic focal points accentuate a preferential tilt towards sectors known for structural advantages, such as technology, pivoting around stalwarts like Microsoft, Nvidia, and Alphabet. Emphasis is also on sectors that promise defensiveness and consistent dividend yields, alongside a vigilant posture towards guidance issued by companies, seeking quality and steering clear of high-beta cyclical stocks amidst tariff-inflicted volatility.

The narrative for Q2-2025 weaves caution with optimism, underscoring a deceleration in earnings growth and keen anticipation for corporate guidance. While underlying fundamentals, particularly in resilient sectors, offer a glimmer of hope, overarching economic indicators and policy stances, especially those by the Federal Reserve, pose challenges.

As investors navigate through these tumultuous waters, the wisdom lies in gravitating towards quality, maintaining a defensive stance, and remaining astute to shifts in corporate outlooks, thereby enabling a balanced risk-reward equation as the earnings season unfolds.

In a realm where fiscal prudence intersects with strategic foresight, the unfolding earnings season is not just a reflection of past performances but a harbinger of economic sentiments that could shape future market trajectories. Investors, thus, are poised at a crucial juncture, ought to tread cautiously yet confidently, steering through the impending fiscal disclosures with an informed lens. Trade with discernment.