In the forthcoming week, the financial world is set to transition into a period marked by intense scrutiny and anticipation as the second quarter of 2025 earnings season commences. This period is highly anticipated due to the comprehensive financial updates provided by an array of corporations, with an initial focus on the prominent banking institutions situated on Wall Street, scheduled for Tuesday and Wednesday. Earnings reports are a cornerstone of the stock market, significantly influencing investor sentiment and expectations by providing a tangible reflection of a company’s financial health and future prospects.

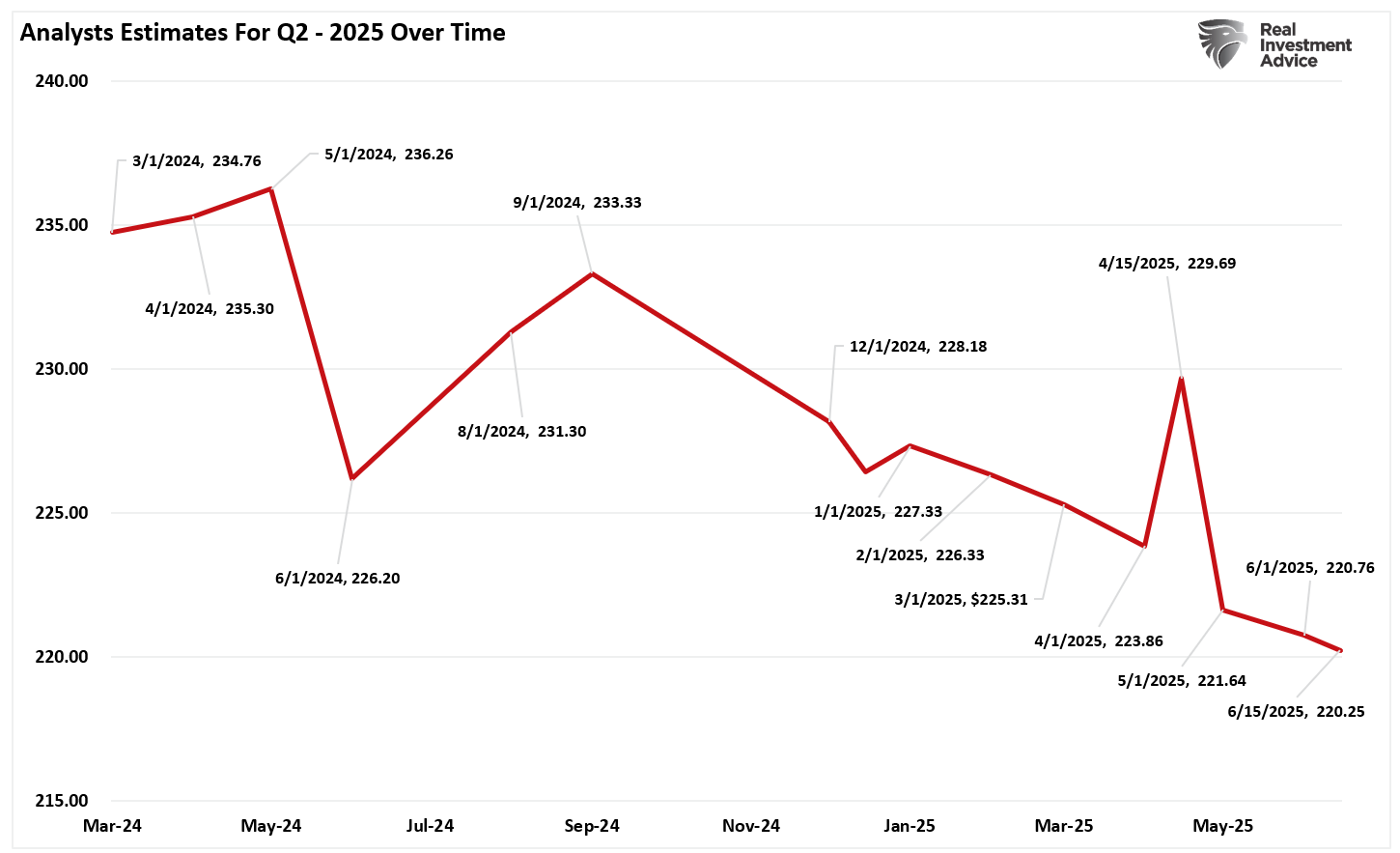

In the preceding months, data sourced from S&P Global has depicted a notable adjustment in the earnings forecasts for Q2-2025. Initially projected at $234 per share in March 2024, these forecasts have been revised downward to $220 per share as of June 15th. This $14 reduction can be largely attributed to apprehensions concerning tariffs and their subsequent impact on corporate outlooks, highlighting the sensitivity of financial markets to geopolitical and economic policies.

A report from FactSet further delineates this trend, stating that analysts have curtailed their earnings expectations for S&P 500 companies for the second quarter beyond the norm. Despite this, the proportion of S&P 500 entities issuing negative earnings guidance is below average. Consequently, current estimations for the S&P 500’s second-quarter earnings are subdued compared to initial expectations at the quarter’s outset. Moreover, these adjustments forecast the S&P 500 to exhibit its minimal year-over-year earnings growth rate since Q4 2023, standing at 4.0%.

This period of revision and anticipation is underpinned by a trio of primary factors: heightened trade risks, notably due to tariff impositions and the uncertainty surrounding their continuation or resolution; diminished consumer spending, reflecting broader economic deceleration; and specific sectoral downturns, with energy and materials sectors reflecting notable declines. These declines underscore the broader economic trends and heighten the importance of corporate earnings as a market barometer.

However, it’s not all pessimistic. The technology and communications sectors are poised to be the bulwark against broader market weaknesses. With substantial investments in artificial intelligence and other capital expenditures, particularly by industry giants referred to as the “Magnificent 7,” robust earnings and revenue growth are anticipated from these quarters. These sectors’ performance could potentially counterbalance the adverse effects arising from trade tensions and consumer spending constraints.

As we edge closer to the unveiling of these earnings reports, the strategic positioning of investors and analysts alike is characterized by a cautious optimism. RIA Advisors, a notable entity in this landscape, delineates its approach towards navigating the upcoming earnings season. Emphasizing a balanced portfolio, the advisors advocate for a focus on sectors with structural advantages, such as technology heavyweights, while suggesting a tilt towards defensive, dividend-paying stocks to mitigate potential risks. Additionally, the tone of company guidance, beyond the raw numbers, is identified as a critical area for scrutiny.

This comprehensive outlook towards Q2-2025’s earnings season encapsulates the complex interplay of economic indicators, corporate performance, and investor sentiment. As we stand on the cusp of these announcements, the financial ecosystem remains attuned to the subtle indicators of economic health and strategic direction provided by corporate earnings. Amidst these dynamics, the underlying fundamentals of key market segments, especially technology and communication, alongside defensive sectors, offer a beacon of stability and potential growth. Nonetheless, the broad consensus among analysts and investors points towards a period of heightened vigilance, with an emphasis on quality, strategic positioning, and an acute awareness of the broader economic trends and policy landscapes that shape the market’s trajectory. This earnings season, thus, is not just a report card on corporate health but a litmus test for the resilience and adaptability of the market amidst ongoing economic and geopolitical challenges.