In the diverse and constantly evolving world of finance and commodities trading, it can be a complex task to discern the movements of the markets at any given time. One of the commodities that has always held a pivotal place in global economics and politics is oil. The recent trends and shifts in oil prices, especially Brent crude, offer a fascinating insight into the broader fabric of international relations, economics, and energy policies.

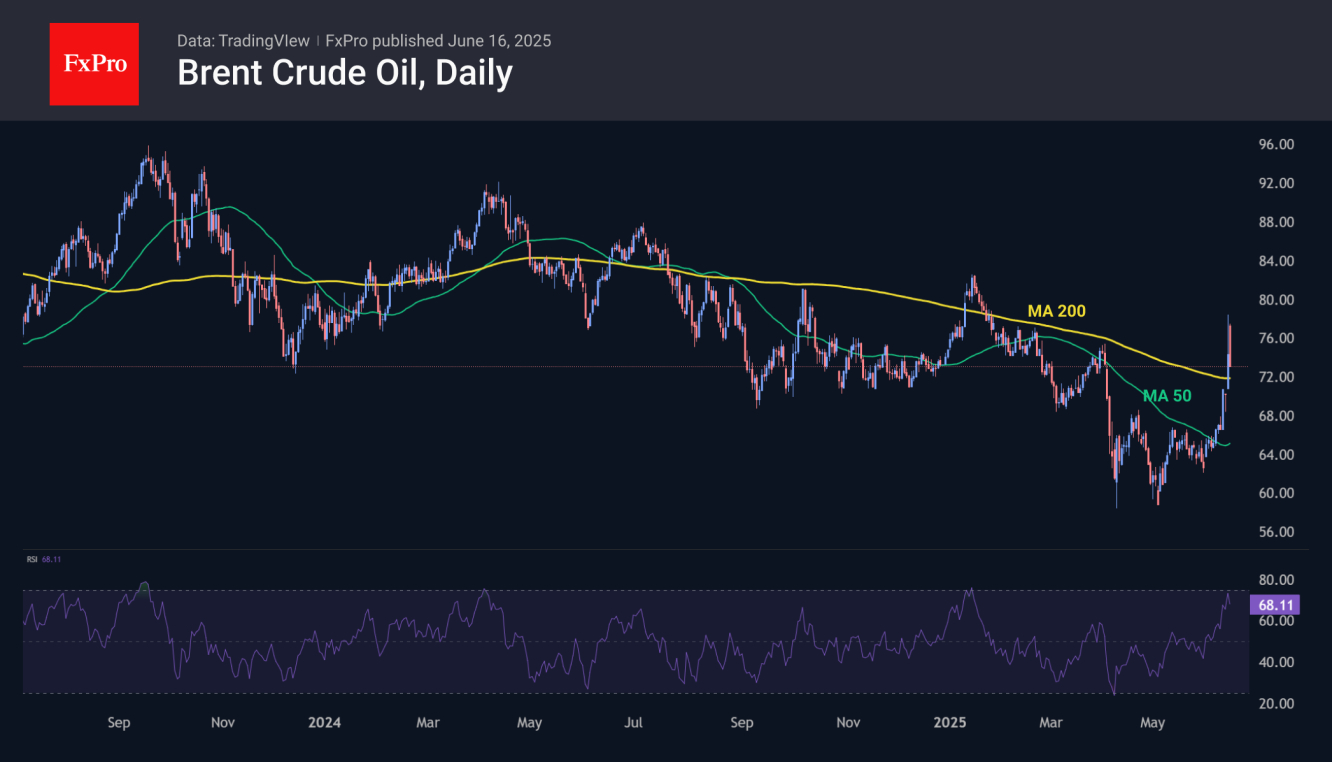

At first glance, given the array of geopolitical events unfolding, one might assume that the stage is set for an upward trajectory in oil prices. Specifically, as of late, there have been significant developments that would traditionally signal a bullish market for oil. However, the reality of the market’s response is somewhat paradoxical. Despite reaching levels not seen since March, Brent crude oil prices experienced a downturn of more than 1% on a Monday compared to the preceding Friday’s closure. This represents a drop of approximately 3.5% from the opening levels the same Monday, indicating a complex interplay of factors influencing the market.

Israel’s recent military actions targeting Iran’s oil and gas infrastructure mark a notable escalation in regional tensions. Iran, on its part, has escalated its rhetoric around potentially blockading the Strait of Hormuz. It’s critical to understand the significance of the Strait of Hormuz in this context. This narrow passage is one of the world’s most crucial chokepoints for the transportation of oil and liquefied natural gas (LNG), with up to 30% of the world’s LNG and 20% of oil passing through it. Any threat to this maritime corridor could have profound implications for global energy supplies and, by extension, prices.

Despite these geopolitical tensions, the market’s reaction was unexpectedly subdued. Oil prices did not breach the highs of $76.3 per barrel witnessed the preceding Friday. Instead, prices began a descent towards $72.5, which, while still 10% above the week’s starting levels, was not as significant as one might expect given the situation’s gravity.

This phenomenon can be partially understood through the lens of recent history. For instance, the market’s response to President Trump’s global tariffs announcement in April, which saw a 22% plummet in oil prices from around $75, starkly contrasts with the current situation. Such volatility underscores the market’s complex response mechanisms to geopolitical and economic stimuli.

It appears that the market is not rushing to factor in a risk premium, possibly due to a growing influence of macroeconomic factors over prices. In contrast to the 1980s, when energy was frequently used as a geopolitical weapon, recent years have seen a trend of oil and gas being the targets of sanctions primarily by importing nations. This shift reflects a broader transformation in how energy commodities are intertwined with global politics and economics.

An additional dimension to the current oil market scenario is the trend of declining drilling activity in the United States. Recent data from Baker Hughes highlighted a decrease in the number of operational oil rigs, bringing the count down to 439, the lowest since October 2021. This reduction in drilling activity could have implications for supply and, consequently, prices.

Despite these variables, the market saw a momentary bullish signal with the closing prices last week surpassing the 200-day moving average, currently at $71.50. However, the sharp decline seen on Monday casts doubt on the sustainability of this trend, suggesting it might have been a short-lived surge influenced by factors such as a short squeeze, wherein large market players capitalize on high-profile news to sell oil to retail traders, thereby influencing market dynamics.

The Relative Strength Index (RSI), a technical oscillator, mirrored peak levels from the past two years at 75 on a daily timeframe, typically indicative of the upper limits in oil prices. Coupled with last week’s surpassing of a former strong support level that had been consistent over three years, the market seemed poised for a bullish phase. Nevertheless, the prompt selling pressure indicates a potential upper hand for bearish forces, using the recent surge as an opportunity to sell.

Understanding these dynamics requires an appreciation of the multifaceted factors at play within the oil market—ranging from geopolitical tensions, macroeconomic influences, to technical trading indicators. The delicate balance between supply and demand, geopolitical strife, and market sentiment contributes to the intricate tapestry of the global oil trade. As events continue to unfold, the oil market remains a critical barometer of broader economic health and geopolitical stability.