The recent trajectory of the dollar, often seen as a global linchpin in financial marketplaces, has notably maintained its downward trend. This descent has been magnified in the context of crises in the Middle East, which, though briefly lending support to the currency, have ultimately seen the dollar’s fortifications eroded, sparking discussions around a crucial pivot toward 1.20 against the euro.

The situation in the Middle East briefly spotlighted the perceived vulnerability of the US dollar. Under normal circumstances, a surge in geopolitical risk coupled with a rise in oil prices might have propelled an undervalued dollar to ascend dramatically. However, the anticipated rally was minimal both in magnitude and duration. This phenomenon underscores a broader sentiment within the highly anticipatory foreign exchange markets, which did not fully account for the ramifications of a drawn-out conflict or sustained elevation in energy costs. Furthermore, a prevailing reluctance to invest in dollars, based on medium-to-long-term forecasts, played a part in this subdued response, highlighting a delicate balance in short-term valuation adjustments.

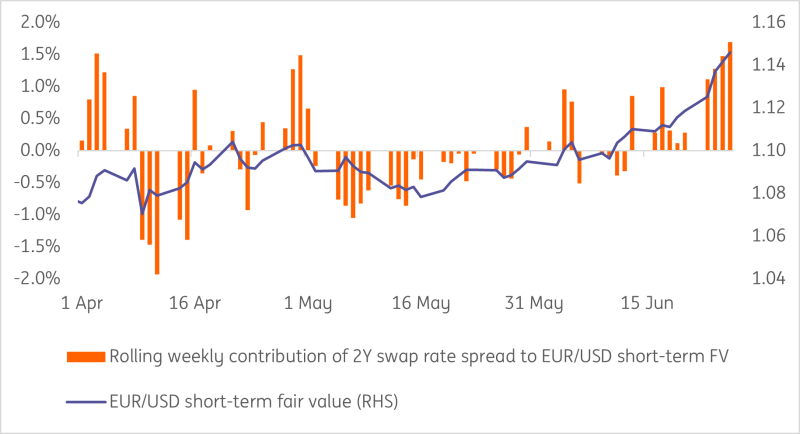

In recent developments, there has been a notable shift in the factors influencing the EUR/USD exchange rate. Analysis suggests that the estimated fair value of EUR/USD has experienced an upward adjustment, moving from just below 1.10 to 1.145 within a fortnight. This adjustment can largely be attributed to a tightening in the EUR/USD swap rate gap, which has swung in favor of the euro, reflecting market projections of a divided Federal Open Market Committee (FOMC) exhibiting dovish tendencies, in stark contrast to a more hawkish stance from the European Central Bank (ECB) which has lent support to euro rates at the front end.

This recalibration of risk premium — previously pegged at around 2.5% when EUR/USD was trading at 1.170, down from 3% at 1.160 — points toward a reduced misalignment in currency valuation, notwithstanding a history of persistent overvaluation observed since what has been colloquially dubbed as ‘Liberation Day’. It implicates that a re-assessment of USD risk premium, to levels previously seen, could potentially edge EUR/USD precariously close to the 1.20 threshold.

A closer inspection of potential catalysts capable of inciting a further depreciative shift in the USD primarily identifies tariffs and US deficit concerns as key triggers. Overlapping timelines — with notable policy decisions like the One Big Beautiful Bill expected to clear the Senate by the 4th of July and the expiration of a 90-day reciprocal tariff pause shortly thereafter — accentuate these risks. Additionally, apprehensions surrounding the autonomy of the Federal Reserve, fueled by speculations of President Trump contemplating a replacement for Chairman Jerome Powell, cast a long shadow over dollar valuations.

In a recent development that has stirred the financial circles, the tentative reassessment of the Federal Reserve’s stance has ushered in a more dovish outlook, further bolstering the EUR/USD fair value. This recalibration is mirrored in the increased FX hedging activities noted in USD-denominated assets, as investors and central banks explore alternatives amidst policy-induced volatilities. Such strategic shifts underscore a possibly enduring risk premium attached to the dollar, notwithstanding the impact of traditional valuation drivers.

Looking ahead, although we remain wary of the European Central Bank’s policy trajectory, with a potential rate cut by September appearing underpriced, the immediate future of EUR/USD dynamics may well hinge on the forthcoming economic data and Federal Reserve discourse. Anticipated dovish recalibrations by the Fed, set against a backdrop of unwavering ECB policy pricing, may well nudge the EUR/USD exchange rate towards the debated 1.20 marker, although this pathway is fraught with conditionalities and market sensitivities.

In synthesizing the current market narrative with evolving geopolitical and policy undercurrents, it seems the optimism surrounding an imminent Federal Reserve rate cut, spurred on by mounting dovish expectations, might not suffice in catalyzing a sustained rally towards 1.20 for EUR/USD. Such a prognosis rests on tangible movements in US dollar risk premia, hinging on developments spanning tariffs, fiscal deficits, and the sanctity of Federal Reserve independence — factors that, while influential, do not form the crux of our projected scenario.

It is palpable that themes underpinning the dollar’s diminishing reserve currency appeal, and the uptrend in USD hedging, are deeply ingrained within the market’s consciousness, capable of invoking asymmetrically negative reactions to unfolding events. However, whether these elements alone can propel EUR/USD appreciably higher remains a subject of speculation.

As we traverse these multifaceted dynamics shaping currency markets, it is imperative to approach the discourse with a nuanced understanding of underlying risk factors and policy shifts, recognising that the current financial ecosystem is a complex interplay of geopolitical, economic, and operational contours that defy simplistic narratives.