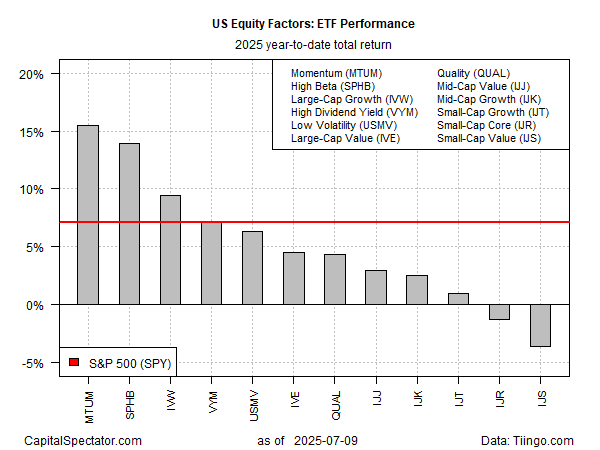

In an ever-evolving landscape of financial currents and commercial tides, the dynamics of economic news throughout the year have been nothing short of whirlwind. Amidst this fluctuating economy and the complex maze of financial markets, a standout phenomenon has been the robust performance of the momentum equity risk factor. This particular factor has charted a commendable course, triumphantly outpacing its counterparts as well as the broader United States stock market panorama, as illustrated by a particular array of Exchange-Traded Funds (ETFs) analysed up to the conclusion of the previous day’s trading session, dated July 9, in the year under discussion.

The iShares MSCI USA Momentum Factor ETF, trading under the ticker symbol on the New York Stock Exchange, has showcased a stellar ascension, clocking in an increase of 15.5% as we traverse 2025 thus far. This impressive surge not only eclipses the performance of other factors in the running but also more than doubles the yield of the encompassing stock market for the same period, as benchmarked by the S&P 500 ETF Trust.

In what could be termed as a financial rollercoaster, the month of April witnessed a dramatic series of events, colloquially dubbed the “tariff tantrum”, which saw the said Momentum ETF (MTUM) along with the broader market, enduring significant hits. Nonetheless, the rebound was swift and vigorous. The MTUM, in particular, recuperated with commendable speed and vigour, surpassing other contenders and firmly positioning itself to relish the gains of this recuperation with an optimistic outlook for 2025.

Emerging from the tumultuous sell-offs in April, another factor-focused fund has made a remarkable recovery, steadily inching closer to challenging MTUM for the coveted position of the year-to-date performance leader. The Invesco S&P 500 High Beta ETF, also trading on the New York Stock Exchange, now boasts a noteworthy upturn of 13.9% in 2025, claiming the second spot in factor performance. Initially aligned or slightly lagging behind the broad market as measured by the S&P 500 ETF Trust (SPY), the High Beta ETF has seen a pronounced acceleration in its comeback over recent weeks. This surge is highlighted by its performance over the past month, where it outpaced the MTUM by a significant margin, recording a 9.2% bounce in contrast to MTUM’s 3.0%. Such momentum may well be a harbinger of a shifting leadership in the ongoing battle of factor performances as we edge closer to the latter half of the year.

Invesco’s strategy for its “high beta” proposition is predicated on aligning with the S&P 500 High Beta Index, which meticulously selects securities demonstrating the highest sensitivity to market movements — encapsulated by the term ‘beta’ — over a trailing twelve-month period. Beta itself is understood as a metric of comparative risk, depicting the rate at which a security’s price evolves. Both the Fund and the Index undergo a quarterly recalibration and restructuring, a ritual conducted in the months of February, May, August, and November.

Based on recent developments and historical performances, there’s a growing anticipation that the Invesco S&P 500 High Beta ETF may ascend as the budding frontrunner in the ongoing contest for factor performance supremacy in 2025. This narrative shines a light on the intricate dance of market dynamics, underscoring the ever-present potential for change and the pivotal role of strategic investment decisions in navigating the financial currents of our times.

This exploration into the performance of specific equity factors underscores not just the resilience and potential of the momentum and high beta strategies within the broader context of the US stock market but also offers a glimpse into the nuanced strategies investors might leverage in their quest for superior returns. As the financial landscape continues to evolve, understanding these dynamics becomes paramount for those looking to navigate these turbulent markets successfully.