As we find ourselves in July, a glance back to March reveals a collective anticipation that the turbulence stirred by President Donald Trump’s trade policies—dubbed Trump’s Tariff Turmoil (TTT)—would have settled by the summer’s end. There was a widely held belief that President Trump would have begun to tout his achievements in the ongoing trade skirmishes with global partners, thereby shifting his focus to other matters more pressing, in an effort to avert a potential recession in the United States. This strategic pivot was deemed crucial, particularly with the looming congressional mid-term elections, as Trump’s administration aimed to bolster the economy to ensure the Republican Party maintained its slender majorities in both the House of Representatives and the Senate come November 2026.

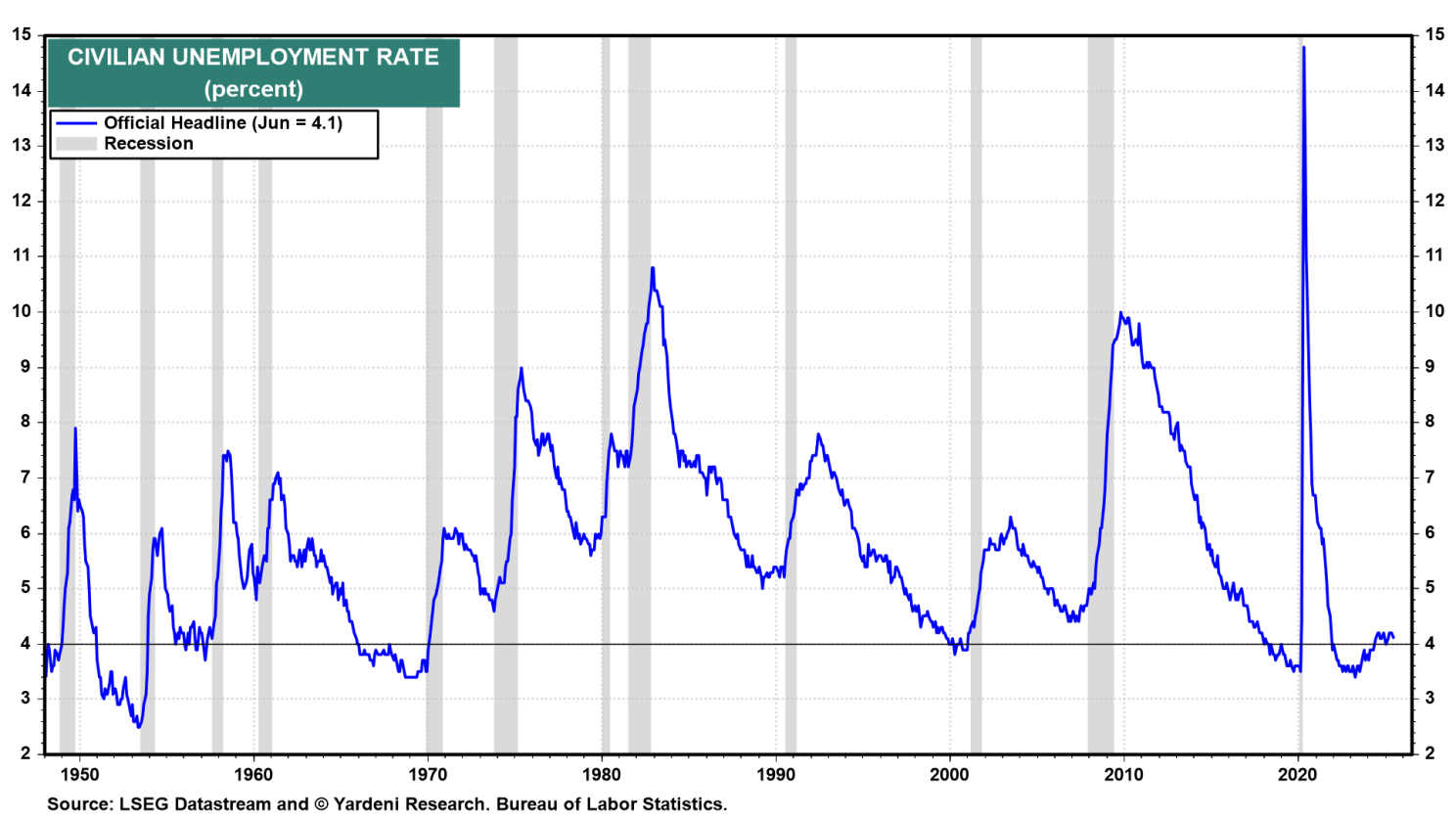

At present, the American economy is performing robustly. The job market is thriving, with unemployment rates hitting a low of 4.1%, while core inflation rates—excluding a gradual decrease in rent inflation—remain under 2% year-over-year. The Misery Index, which combines unemployment and CPI inflation rates, stands at a comfortable 6.6%, markedly lower than its historical average of 9%. Such economic indicators lead to the question: Why would Trump risk destabilizing this success with further trade confrontations? It seemed logical that he might instead leverage this economic prosperity and geopolitical achievements as a platform to support Republican candidates in the forthcoming elections.

In the context of financial markets, on March 13, amidst the unfolding tariff narrative, we adjusted our year-end target for the S&P 500 downwards to 6400 from an optimistic 7000, despite maintaining a bullish stance—as evidenced by the S&P’s close at 5521.52 before the adjustment. This revision was couched in cautious optimism, predicated on the assumption that Trump would temper his tariff strategies to sidestep economic downturns that could jeopardize Republican control in Congress during the late 2026 elections.

By the end of March, further adjustments saw our target lowered to 6100 as Trump’s April 2 ‘Liberation Day’ approached—a date which heralded intensified trade maneuvers but even this revised target was approached with a bullish outlook. Come April 7, we predicted a potential market correction bottom, expecting a shift in Trump’s trade policies following significant market reactions. The hope was for a brief pause in tariff increases to allow for fruitful trade negotiations.

Indeed, the stock market witnessed a temporary recovery, hitting a record high on July 3. However, Trump’s stance on tariffs intensified once more with plans to implement reciprocal tariffs on various nations starting August 1, unless trade negotiations yielded favorable outcomes for the US. This reciprocal tariff threat extended to countries such as Canada and Brazil, alongside proposed heavy tariffs on goods from the European Union and Mexico and a staggering 200% on pharmaceuticals—though these were potentially delayed subject to negotiation periods.

This pivot back to aggressive trade policies underscores a recurring pattern in Trump’s approach: a willingness to leverage high-stakes tariffs as a negotiation tool, believing it strengthens the US’s economic posture while concurrently providing a platform for declaring trade victories domestically. This strategy, however, comes with significant risks, including potential backlash against American exporters and increased prices for consumers—thus indirectly taxing American citizens and companies.

Financial markets, however, have displayed remarkable resilience in the face of escalating trade tensions, potentially due to a belief in Trump’s negotiation tactics leading to beneficial trade agreements. However, as the administration pushes forward with its tariff agenda, it’s clear that the repercussions on global trade, market sentiment, and the broader economy remain uncertain.

In the broader context of Trump’s economic strategy, there lies a delicate balance between leveraging tariffs as a negotiating tool and ensuring they do not backfire by hampering economic growth or precipitating a market downturn that could erode the public’s confidence in Republican leadership as the mid-term elections approach.

With the policy landscape in flux and markets reacting in real-time to developments on the trade front, stakeholders—from investors to policymakers—must navigate these uncertain waters with both caution and an eye towards the long-term implications of today’s decisions on tomorrow’s economic and political realities.