In the intricate weave of the investment landscape, a diverse portfolio stands as a bulwark against the unpredictable tides of market fluctuations. As we ride the crest of a buoyant equities market, it behoves the astute investor to cast their gaze beyond the horizon of stocks to explore additional vessels of investment, such as bonds or Real Estate Investment Trusts (REITs). These alternatives not only offer the potential for risk mitigation but also hold the promise of enhancing dividend returns, a strategy of paramount importance in the current financial milieu.

Our exploration of this topic in last Thursday’s discourse unveiled a straightforward approach to achieving portfolio diversification while securing an appealing 7.9% dividend yield. If you haven’t had the opportunity to peruse that insight, I encourage you to acquaint yourself with those valuable perspectives.

Venturing deeper into the realm of income-generating investments, closed-end funds (CEFs) emerge prominently, particularly those invested in municipal bonds. These bonds, often referred to as ‘munis’, are financial instruments issued by local and state governments to fund public infrastructure projects. A notable attribute of munis is their capacity to offer tax-free dividends to a majority of American investors, rendering them an attractive option for income-focused portfolios.

Our discussion today pivots around the nuanced landscape of muni-bond CEFs, highlighting the pivotal role of timing in maximizing returns from these instruments. For instance, an evaluation reveals a significantly overvalued muni-bond CEF poised for a downturn, in stark contrast to another offering a 7.4% dividend yield and currently trading at a commendable discount—nearly 10% below its intrinsic value.

The appeal of muni-bond CEFs is magnified when one considers their tax advantages. To illustrate, a muni-bond CEF yielding an approximate 8% in our ‘CEF Insider’ portfolio might actualize a taxable-equivalent yield of 13% for certain investors, based on their tax bracket. Such a yield transformation underscores the financial efficacy of these instruments in a well-curated investment portfolio.

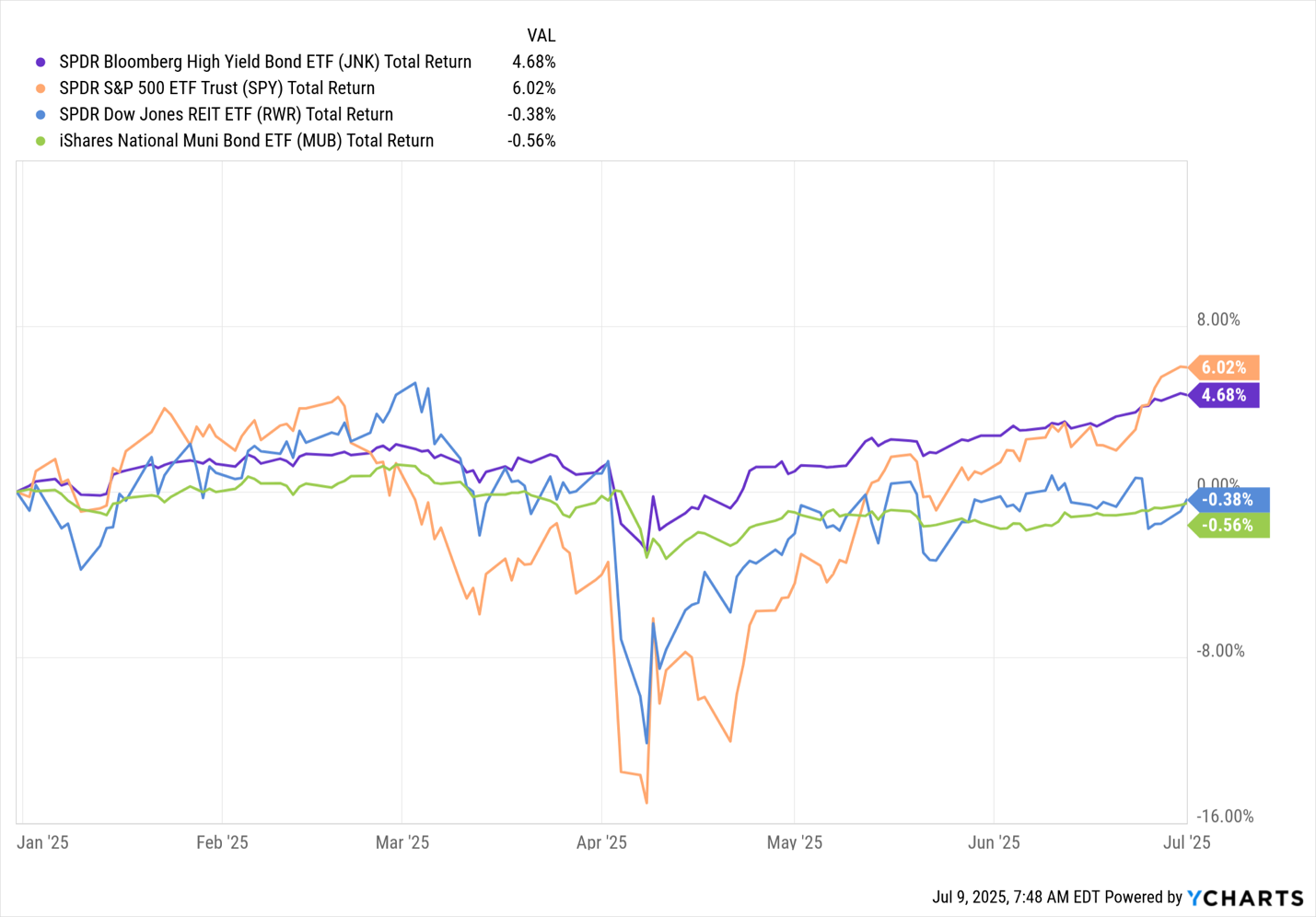

Despite their allure, our current engagement with muni-bond CEFs is selective, motivated by their performance relative to other investment classes such as high-yield bonds and REITs. Indeed, munis have lagged behind their counterparts through the initial half of the year. However, the landscape is dynamic, with the resurgence of the S&P 500 marking a potential shift in investor sentiment towards seeking stable, high-yield, and tax-efficient alternatives amidst fears of a stock market correction.

Historical patterns offer insight into the cyclical nature of the muni-bond market. For example, the period of market tumult from 2007 to 2009 saw muni bonds holding steady initially, only to surge in the aftermath of the 2008 market downturn, delivering substantial returns. Such patterns suggest the potential for munis to outperform during periods of market volatility.

Fast forward to the first half of 2025, and we observe an echo of the past, with stock markets rebounding amidst sustained economic growth. This resilience of the economy, which we have emphasized at ‘CEF Insider’, has led us to adopt a cautious stance towards muni-bond CEFs.

Nonetheless, some muni-bond CEFs have garnered extraordinary investor interest, as evidenced by the Invesco California Value Municipal Income Trust. This fund has oscillated between substantial discounts and premiums to its Net Asset Value (NAV)—at times trading at nearly a 5% premium, indicating investors are willing to pay above the portfolio’s worth.

This discrepancy between the fund’s market price and underlying NAV raises concerns, particularly when the premium is not justified by NAV growth. Such scenarios warrant a reevaluation of investment positions, despite the fund’s strong management and the robust tax revenue growth in California buoyed by sectors like technology and media.

Given the prolonged underperformance of munis relative to other investment classes, coupled with the stock market’s recovery, the case for investing in underpriced muni-bond CEFs becomes compelling. Enter the abrdn National Municipal Income Fund, an investment vehicle offering a 6.2% yield at a 10.3% discount to NAV. This anomaly—an offering from a diversified and traditionally secure asset class trading at a significant discount—signals a rare opportunity for investors.

In conclusion, while the allure of munis, particularly tax-advantaged muni-bond CEFs, remains undiminished, the prudent investor will exercise discernment in timing and selection. The landscape is ripe with opportunities, where the judicious choice of underpriced muni-bond CEFs could significantly enhance the income component of one’s portfolio.

Disclosure: Brett Owens and Michael Foster remain committed to uncovering undervalued stocks and funds across the U.S. markets, leveraging contrarian income strategies to identify opportunities for robust dividend growth. For insights into profiting from their approaches, consider exploring their latest report, “7 Great Dividend Growth Stocks for a Secure Retirement.