Participating in the global financial arena, the eyes of investors and analysts worldwide are turned towards Jerome Powell, the Chairman of the Federal Reserve, as he prepares to address the Jackson Hole Symposium this week. This event occurs amidst a landscape of swift alterations in expectations concerning the Federal Reserve’s monetary policy, sparked by data from July that hinted at a diminished likelihood of significant interest rate hikes. The anticipation surrounding the September meeting has consequently narrowed and become more precise.

A cautious stance by Powell might lead to the strengthening of the US dollar against a basket of major currencies. This is especially pertinent because there still exists a palpable expectation for considerable rate reductions in the future. A message of careful consideration could potentially amplify the US dollar’s position.

Delving into the intricacies of how the Federal Reserve could navigate the conundrum of inflation juxtaposed with employment presents a complex scenario. The American economy has been emitting mixed signals; robust consumer activity points towards a strong economic appetite, while the escalation in import prices—exacerbated by tariffs—signals rising costs. This delicate balance poses the risk of inflation, a phenomenon that could cascade into retail prices shortly. The employment sector has not been spared, showing a marked downturn. A weakening job market, characterized by a three-month average unemployment rate that has escalated to 4.2% and a deceleration in new job creation, underscores the challenges.

Rewinding to the previous year, Powell, confronted with a somewhat similar scenario, hinted at an impending rate cut during his speech at Jackson Hole. The current circumstances, however, are steeped in complexities. With inflation rates witnessing a sharp increase to 3.5%, and core inflation tagging closely behind at 3.7%, the Federal Reserve stands at a crossroads, making rapid decisions a herculean task.

Amidst these economic tumults, Powell might adopt a path of caution and flexibility in the year’s policy adjustments, emphasizing vigilant monitoring of both employment and inflation trends, recognizing the intricate dance between stimulating economic growth while keeping inflation in check.

On a different note, geopolitical events, particularly a meeting between US President Donald Trump and Russian President Vladimir Putin, have also been a pivot point for the US dollar’s fate. An agreement by Putin to allow security guarantees for Ukraine, reminiscent of NATO’s Article 5, has sparked a glimmer of hope towards resolving the Ukraine crisis. However, the shadow of unresolved demands over Donbas and Crimea looms large, potentially damping the prospects for peace.

From a market perspective, this geopolitical development can sway the US dollar’s trajectory dramatically. The optimism of an imminent ceasefire might reduce the US dollar’s appeal as a haven, whereas faltered negotiations or a deadlock could boost its safe-haven allure.

Market expectations, especially within the interest rate corridors, have seen a recalibration—from a once dominant belief in a 50 basis point cut in September to a more conservative estimate below 25 basis points. This shift underscores a broader skepticism about the Federal Reserve’s willingness to take drastic monetary actions.

Investors are on tenterhooks, keen to see how Powell navigates these expectations. If his articulation at Jackson Hole underscores the gravity of inflation and the risks of hasty policy shifts, the US dollar index might witness an uptick. Conversely, a narrative focusing on employment fragilities could dampen the index.

As Powell steps up to the podium at Jackson Hole, he does so at a crucial juncture, with the power to sway the US dollar in global markets profoundly. The outcome will reflect the Federal Reserve’s stance on critical issues—the balance between interest rate policy, ongoing US-Russia-Ukraine peace talks, and the intricate dance between inflation and employment within the US economy.

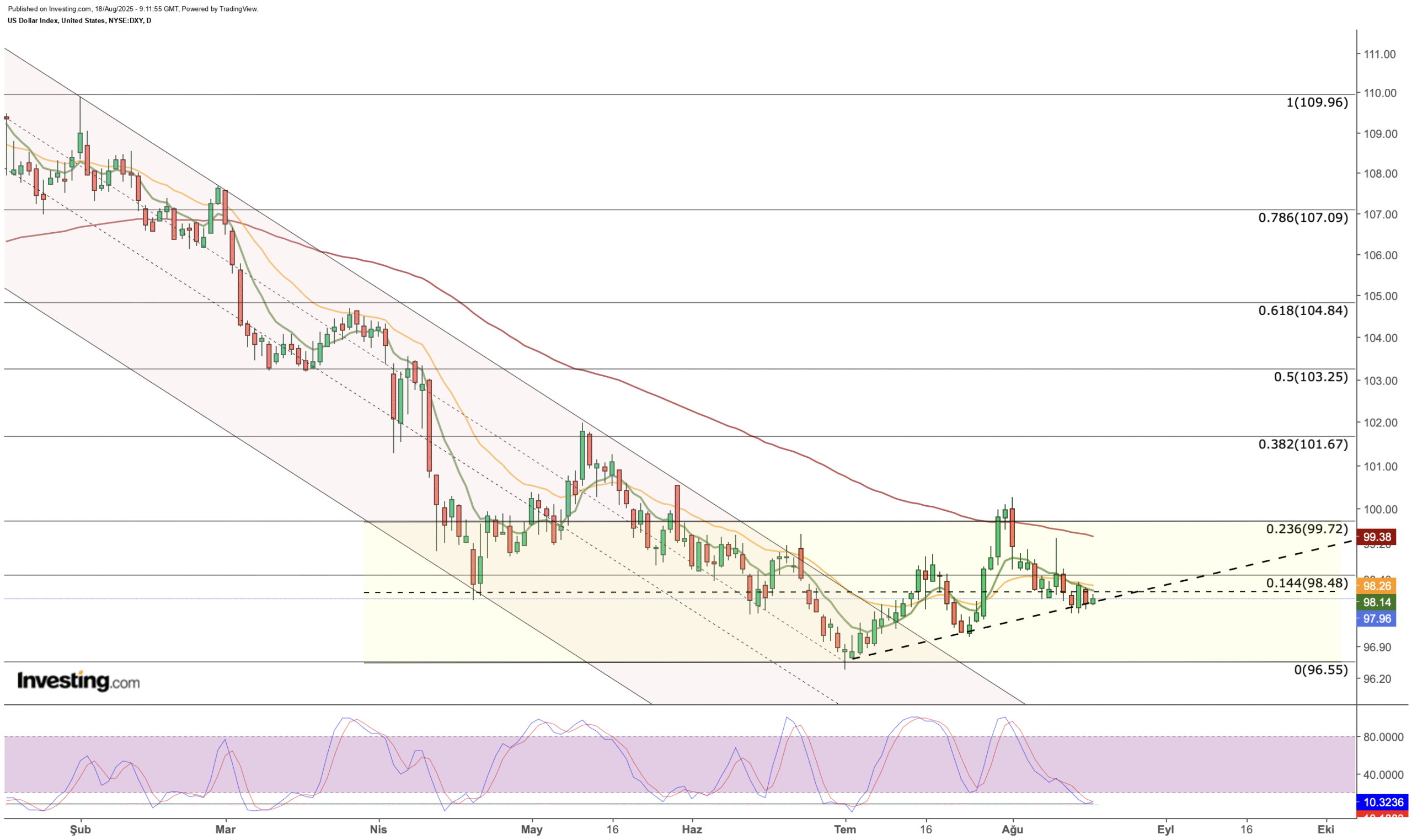

The forthcoming days are poised for potential pivotal movements between 97 and 99 on the US dollar index. A cautious approach by Powell could fortify the US dollar, propelling it towards the 100 threshold, exerting pressure on emerging market currencies. Alternatively, a focus on employment over immediate rate cuts could see the index dip below 97, potentially buoying gold prices and riskier asset classes.

In this nuanced global economic dance, the directions taken by Jerome Powell and the Federal Reserve are much more than mere policy choices. They are signals, harbingers of economic sentiments and strategies that will shape the financial landscape, offering a blend of challenges and opportunities to investors and policymakers alike.

The interplay of economic policies, geopolitical dynamics, and market expectations creates a rich tapestry of possibilities and uncertainties. As the global community watches, the decisions made and messages conveyed at the Jackson Hole Symposium will doubtlessly play a pivotal role in sculpting the economic narratives for the remainder of the year and beyond.