In the world of finance, the ebb and flow of the stock market are often heralded by significant events and indicators that seasoned investors keep a watchful eye on. One such period of keen interest concluded last Friday, marking the end of the options expiration period—commonly referred to as OPEX. This juncture often forecasts a pivot in market volatility, which had been relatively contained. Following a post-OPEX environment, it’s anticipated that this quietude will give way to more pronounced fluctuations in the market. Particularly, with another OPEX scheduled for the upcoming Wednesday, investors are navigating through what could be considered a transitional phase for the market.

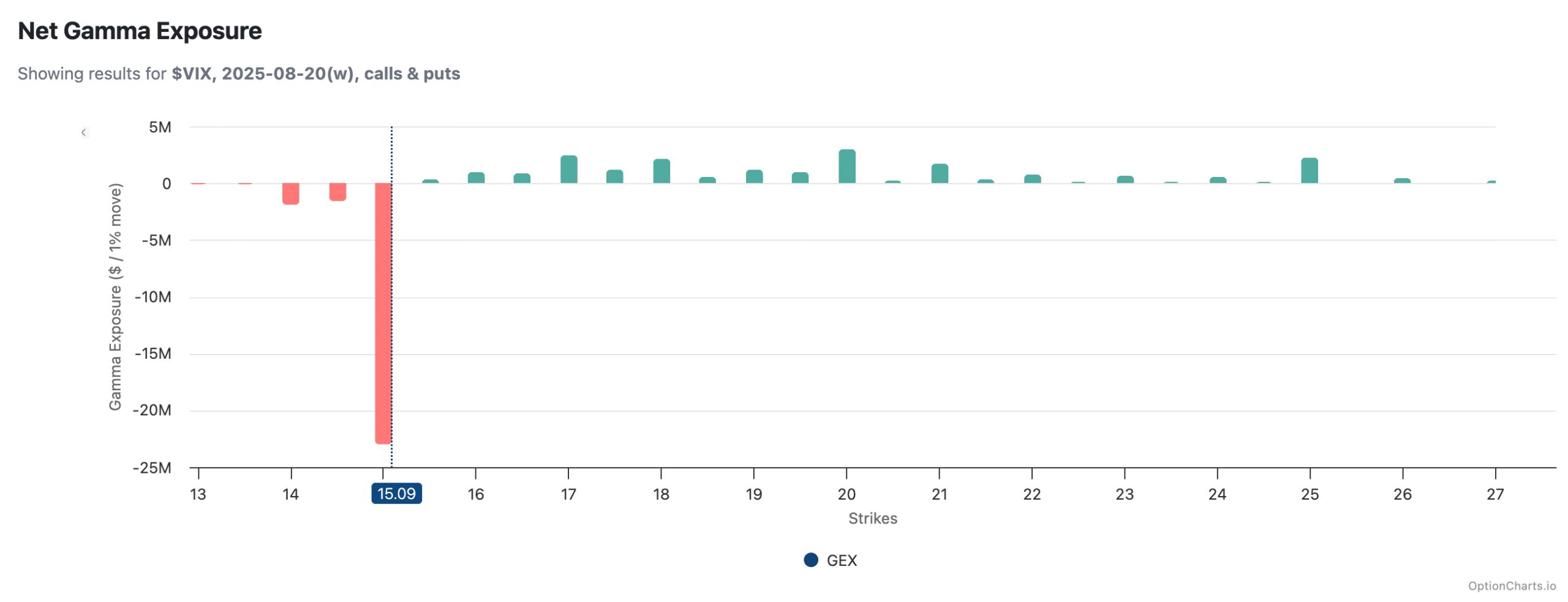

At the heart of market volatility lies the Volatility Index (VIX), often seen as a barometer for market sentiment regarding risk levels. Recently, the VIX has demonstrated resilience, holding steady at a base level of 15. This figure is characteristically referred to as the “put wall,” indicating a threshold below which the VIX is less likely to fall, at least in the immediate days leading up to Wednesday. This steadfastness suggests a market bracing for impending shifts, prepared for the potential upticks in volatility that post-OPEX periods typically entail.

The financial community has now set its sights on the upcoming event in Jackson Hole, which under usual circumstances, serves as a pivotal platform for insights into the Federal Reserve’s forthcoming strategies. Market participants traditionally hang on every word from the Chair of the Federal Reserve, seeking guidance or any indication of shifts in monetary policy. However, the current scenario paints a different picture, with Chair Powell approaching the last six months of his term. With the transition on the horizon, Powell’s influence on market expectations might be perceived as muted, and the market is bracing for a potential shift in leadership and policy direction at the Fed.

Amidst speculations and anticipatory adjustments, a critical question looms large – does Powell retain sufficient backing from the Federal Open Market Committee (FOMC) to maintain steady interest rates? The increasing clamor for rate cuts amongst certain FOMC members adds an intricate layer to this narrative. Speculation abounds that dissent could peak at the forthcoming September meeting, with figures such as Bowman, Waller, and Miran (subject to confirmation) likely leading the charge for a policy shift. Despite this undercurrent of contention, consensus leans towards Powell garnering adequate support to eschew rate reductions. Nonetheless, Powell is at a juncture where conveying the high threshold for rate cuts has become imperative, especially given the market’s inclination towards looser monetary policy. It’s a delicate balancing act between staving off inflation risk and addressing any tangible softening in the labour market.

In tandem with these policy deliberations, liquidity dynamics are under the microscope, with notable fluctuations in the Reverse Repo figures drawing attention. A recent uptick to approximately $34 billion, from a preceding $28 billion, signals a departure from the Repo’s role both as a counterbalance to the Federal Reserve’s shrinking balance sheet and a funding mechanism for Treasury issuances. The Treasury’s mounting debt issuance obligations spotlight an impending liquidity crunch, potentially compelling markets to seek capital injections from alternative avenues such as money markets or the balance sheets of primary dealers.

While reserve balances haven’t shown significant immediate impact, the anticipation is that this week could mark the beginning of tangible shifts. The overarching question for the markets, in the weeks ahead, revolves around the underlying drivers of stock market elevation in recent years. Was it the augmented liquidity courtesy of the reverse repo facility propelling stocks and inflating price-to-earnings multiples, or were these market rallies a product of organic growth and investor confidence?

As the curtain rises on this unfolding economic drama, the narrative is rich with uncertainties, anticipatory strategies, and the quest for stability in a landscape punctuated by the prospect of policy shifts, liquidity challenges, and the inherent volatility of transition periods. The forthcoming weeks promise to serve as a decisive test for the resilience, adaptability, and foresight of the global markets.