In the past week, global financial markets have been navigating through a labyrinth of fluctuating investor sentiment, the looming spectre of macroeconomic pressures, and escalating geopolitical tensions. Amidst this backdrop of uncertainty, the spotlight has inevitably swivelled towards the Federal Reserve, particularly with respect to its latest Federal Open Market Committee (FOMC) meeting. Despite widespread anticipation, the FOMC’s decision to maintain the federal funds rate at a steady 3.9% was largely overshadowed by the nuanced undertones of its forward-looking projections.

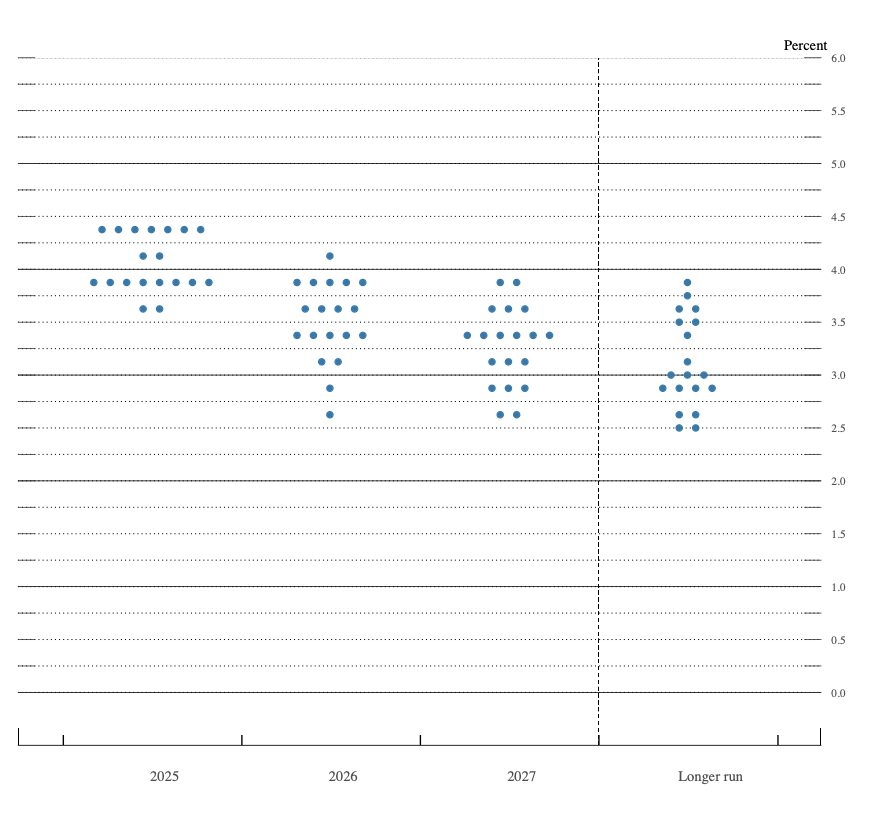

Delving deeper into these developments, it becomes apparent that the Federal Reserve adopts a cautious stance, displaying no immediate inclination towards reducing interest rates, a scenario most market participants might have been yearning for. June’s Summary of Economic Projections painted a picture of tempered expectations for rate normalization. The projections indicate a reduction in real GDP growth predictions for the year 2025 to 1.4%, coupled with an anticipated escalation in unemployment rates to 4.5%. These figures signify a potential deceleration in economic momentum and hint at a cooling labor market.

Moreover, inflation rates, which serve as a critical metric for policy formulation, remain persistently elevated above the Federal Reserve’s 2% target, with PCE inflation forecasted at 3.0% and PCE core inflation at 3.1%. Such persistence in inflationary pressures solidifies the notion that policymakers are not under any immediate pressure to alter their course. This is further corroborated by the projections for 2026 and 2027, which only suggest marginal reductions in interest rates, thereby reinforcing the hypothesis that a 3.0% rate might evolve to become the new normative benchmark for the long term.

This cautious outlook from the Federal Reserve serves as an implicit deterrent against premature risk-on trading behaviors, signaling that any anticipation of a swift policy pivot might be unfounded at this juncture.

The discourse around geopolitical risks merits equal attention. The ongoing tensions in the Middle East have cast a long shadow over global markets, inducing a retreat in European equities and a transient spike in gold prices, while simultaneously stirring a sense of fragility within the cryptocurrency sector. Adding complexity to this scenario, former U.S. President Donald Trump’s ambiguous messages concerning the U.S.’s stance on the conflict have exacerbated market jitters, prompting a knee-jerk reaction evidenced by a dip in oil prices and heightened investor apprehension over potential volatility. Market analysts caution that any overt U.S. military intervention could precipitate a pronounced shift away from risk assets across both equity and cryptocurrency domains.

Amidst this climate of uncertainty, the Fear & Greed Index, a barometer for investor sentiment, currently hovers at a neutral position of 48, epitomizing the market’s ambivalence. Despite the cryptocurrency market capitalization standing at an impressive $3.25 trillion, the Altcoin Season Index suggests a predominance of Bitcoin, with a score of merely 23/100, an affirmation of Bitcoin’s commanding presence in the market.

Turning our gaze towards individual cryptocurrencies, Bitcoin remains mired under the $105K threshold, with the market demonstrating a lack of strong conviction necessary for a bullish breakout. Conversely, Ethereum exhibits a relative robustness, consistently navigating around the $2,500 – $2,520 price range. This resilience is further highlighted by a temporary flip to negative funding rates before reverting to positive, suggestive of a potential exhaustion in short interest – a widely recognized precursor for a trend reversal. However, it’s imperative to acknowledge that without significant inflows, such movements might merely result in a temporary bounce rather than a sustained breakout.

Looking ahead into the upcoming week, the confluence of steadfast monetary policy, persistently high inflation, intensifying geopolitical tensions, and tentative cryptocurrency consolidation paints a complex picture for market participants. While a decisive breach of the $105K mark by Bitcoin could reignite momentum, Ethereum’s nuanced indicators of potential upward rotation warrant close observation, especially if funding dynamics and inflows align favorably.

However, the overarching narrative remains dominated by macroeconomic and geopolitical developments, particularly those emanating from the Middle East. The trajectory of markets in the near term is likely to be significantly influenced by the resolution or escalation of these tensions.

In conclusion, as we navigate through these tumultuous waters, the confluence of monetary policy steadiness, geopolitical uncertainties, and mixed signals within the cryptocurrency markets underscores the importance of vigilant market analysis and informed decision-making. It’s a reminder of the intricate interplay between global events and financial markets, urging both seasoned and novice investors to tread cautiously in this volatile landscape.

Please note: This discussion is intended purely for educational purposes and should not be construed as investment advice. As always, conducting one’s own research (DYOR) is paramount, especially in the high-stakes environment of cryptocurrency investing, where market risks and volatilities are pervasive. Proceed with caution and diligence.Consumer Price Index (CPI)